E-RATE INDIANA FIBER DIA Pricing

What the Map4.net / USAC data shows

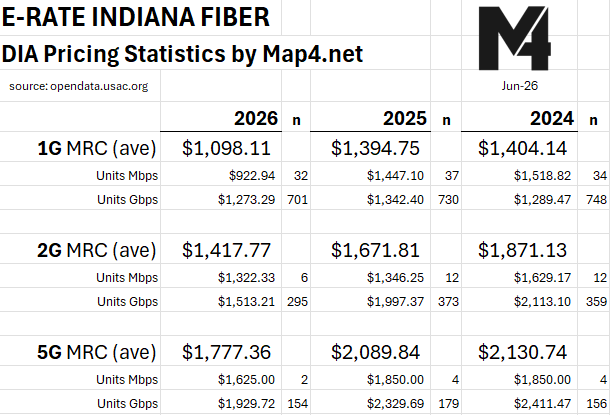

Your report (sourced from opendata.usac.org) documents clear year-over-year declines in average Monthly Recurring Charges (MRC) for Dedicated Internet Access (DIA) over fiber in Indiana E-Rate applications:

1G MRC (average): ~$1,404 (2024) → ~$1,395 (2025) → $1,098 (2026) — a sharp ~21% drop.

2G MRC (average): ~$1,871 (2024) → ~$1,672 (2025) → $1,418 (2026) — steady declines.

5G MRC (average): ~$2,131 (2024) → ~$2,090 (2025) → $1,777 (2026) — also down noticeably.

The sample sizes ("n") are robust (hundreds of circuits), and the breakdowns by "Units Mbps" vs. "Units Gbps" likely reflect different provisioning or quoting conventions in the underlying USAC data. These are pre-discount prices that E-Rate applicants see in bids/commitments.

Provider cost trends: Build vs. "light and operate"

Fiber deployment / CapEx (the big one) is not decreasing. The authoritative 2025 Fiber Deployment Cost Annual Report from the Fiber Broadband Association (FBA) and Cartesian (surveying operators and contractors across 38 states) shows:

Median underground deployment: $18 per foot in 2025 (+3% year-over-year).

Median aerial deployment: $8 per foot (+14% year-over-year).

92% of respondents reported higher costs in 2025; 88% expect increases again in 2026.

Primary drivers: Labor (65–72% of total cost, with skilled splicers and crews in short supply and higher wages), materials (tariffs/inflation), permitting delays, and make-ready work (pole preparation). Underground is more than 2× aerial.

Midwest costs are relatively better than the West (e.g., aerial Midwest median around $6.55/ft vs. higher elsewhere), but the upward trend is national. Some efficiency tools help (pre-terminated cables, microtrenching, overlashing, internal crews saving ~10%), but they are not enough to offset the rises.

The cost to provide lit DIA service (electronics + operations) has more positive dynamics. Once fiber is in the ground (or expandable), modern networks deliver very low marginal cost for additional lower-speed circuits like 1G/2G/5G:

Optical technology is improving rapidly: coherent pluggables (e.g., 400G/800G ZR/ZR+), silicon photonics, photonic integrated circuits (PICs), and higher-density DWDM allow one fiber pair + modern transponders to carry far more capacity with lower power, fewer components, and lower cost-per-bit.

1G/10G-class optics are now highly commoditized and inexpensive.

Higher-capacity backbones mean providers can provision school DIA circuits as low-marginal-cost "add-ons" rather than dedicated low-speed systems.

Scale effects from massive U.S. fiber builds (BEAD + private investment) + competition increase on-net/near-net locations and utilization, spreading fixed costs.

In short: Build costs are a headwind (rising), but "lit service" economics are a tailwind (declining per-bit and marginal costs).

Why prices to schools/libraries are falling more noticeably

The 2026 drops (especially the step-change in 1G) likely reflect a combination of:

Heightened competition in Indiana E-Rate bidding — more providers (Joink, Segra, Zayo, local/regional fiber players, etc.) with more fiber in the ground or near schools, leading to more responsive Form 470 bids and aggressive pricing.

Technological leverage — modern high-capacity systems make incremental 1G/5G DIA very cheap to deliver once infrastructure exists.

Market maturation — fiber is becoming more "commodity-like" for these mid-tier speeds in competitive areas; providers can win volume with thinner margins on recurring services while monetizing elsewhere (higher speeds, other verticals, or overall network utilization).

Broader trend: E-Rate Category 1 bandwidth costs per megabit have been on a long downward trajectory nationally as applicants get faster connections at better prices through smarter procurement and competition.

Important caveats: Individual bids still vary enormously based on distance to the provider's network, whether special construction is needed, contract length, existing infrastructure, and urban/rural factors. Averages mask wide dispersion. Special construction (if required) remains expensive and is a separate line item.

Bottom line for E-Rate stakeholders in Indiana

Schools/libraries: Excellent news — lower pre-discount MRCs improve affordability even before the 20–90% E-Rate discount. Tools like Map4.net that surface this data in near real-time give applicants stronger negotiating positions.

Providers/consultants: The build-cost environment remains challenging (labor is the killer). Success comes from being on-net or near-net where possible, leveraging modern optics for low marginal cost, competing aggressively on total cost of ownership (not just MRC), and using data-driven targeting. Volume and utilization matter more than ever.

The customer price declines are real and material, but they are enabled more by competition + tech-enabled low marginal costs than by falling physical build costs.